By: Rujuta Waknis, Vice President of Digital Solutions

Introduction

Today, almost everyone has heard the buzzword “blockchain,” most likely in the context of cryptocurrency, and specifically the most famous one — Bitcoin. Recently, the cryptocurrency crash in 2022 and its reverberations in the investment world have brought the blockchain hype even more into focus.

However, blockchain is not the same as cryptocurrency or Bitcoin. It is the underlying technology that was built to make cryptocurrency possible. As we look beyond cryptocurrencies, this technology has the ability to definitively track any resource of value in a non-centralized manner. The nature of blockchain as a transparent, immutable shared ledger provides a powerful foundation for tracking and reporting about any asset with value — whether physical (land, buildings, vehicles) or nonphysical (currency, payments, intellectual property, grants). Assets can be both commercial (currency, buildings, factory outputs) as well as governmental (grants, taxes, property). Another popular application of blockchain technology has been making the news lately. Non-fungible tokens, or NFTs, are the digital version of content — such as images, videos, music, or art — that can be registered on the blockchain, along with their ownership, and sold or traded as assets of value.

In this blog, we explore the concept of blockchain and how it is used in commercial applications. The next blog in the series will explore the application of blockchain technology in the public sector. The third blog will dive deeper into how blockchain technology can be used in grants management — a domain primed for greater transparency and innovation.

What is blockchain technology?

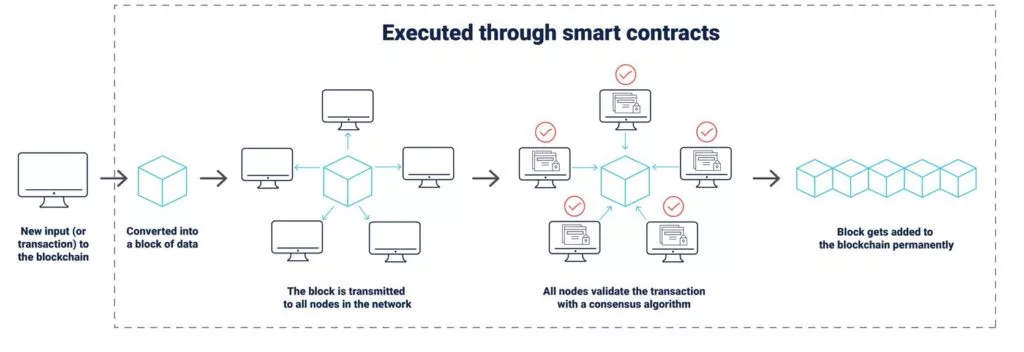

At its core, blockchain is really a distributed ledger technology. A ledger is an accounting document that contains data about assets, transactions, and transaction owners. It is distributed not by being stored centrally on just one server but by having many identical copies stored on many servers in a network.

The asset and transaction data is converted to a hash, which is the fixed-length, encrypted version of the data. The hash forms the basis of the cryptograph (coded message) that scrambles the data such that the only way to read that data is by possessing the keys to the hash. This means hackers and disrupters who don’t have the keys to the blockchain network are not able to read or access the data.

The encrypted data is stored in blocks of information along with a pointer (hash of the header) to the previous block, thus forming a connected, tamperproof chain. And voilà! That forms the blockchain.

The blockchain also has another data structure in it called a Merkle tree. Merkle trees do not store the data, only the hash pointers in a tree formation. Separating the data from the hash allows efficient verification and validation of the data and ensures that the blocks in the blockchain cannot be tampered with (i.e., they are immutable). A great explanation of hashes and Merkle trees is available here.

Figure 1. Components of the blockchain and how a transaction works

Figure 1. Components of the blockchain and how a transaction works

Participants interact with the ledger via nodes in a peer-to-peer network. Nodes form the infrastructure of the blockchain network. Nodes are like individual servers that contain the business rules and conditions to add and validate or confirm transactions. These rules and conditions form the basis of smart contracts, which execute the transaction. For example, a smart contract in a blockchain network for tracking a physical asset or property may be set up to execute the change in ownership of the property when the value of the property (in dollars) has been transferred to the seller.

The ledger is shared and duplicated by all the participants who have nodes in the network. The duplication of data means that tampering with a single copy of the ledger cannot succeed in stealing an asset or its value because many other copies exist, each separately secured in a node.

The immutability of the blockchain means that the sender and receiver of the transaction cannot deny its existence. This is called non-repudiation, and it is a key element in the security and integrity of the data.

Another component critical to the technology is the consensus algorithm. The distributed nature of the blockchain technology requires a method to achieve agreement on the data elements, which is fulfilled by the consensus algorithms. The two most common algorithms are Proof of Work (PoW) and Proof of Stake (PoS).

The original consensus algorithm, PoW, involves confirming that a specific amount of computational capacity (work) has been used to validate transactions. Since this often involves massive amounts of computational hardware, which in turn requires a large amount of energy, it acts as a deterrent to hackers trying to gain access to the encrypted data.

PoS evolved as a consensus algorithm precisely to avoid the large energy requirements of PoW. PoS works by requiring participants to stake tokens for verifying transactions. These tokens, or stake, are used as collateral if the participants act fraudulently.

There are many helpful videos that explain how blockchains and their components work. One of the most popular ones (with over 8.5 million views) is available here on YouTube.

How is blockchain different from existing technologies that can store, view, and send data?

The primary difference between blockchain and traditional business systems is that blockchain’s distributed ledger is decentralized and every participant node in the network has a complete copy of the ledger. The source of truth for each transaction is available to everyone, and there is no single centralized point of ownership.

The other core difference is that transactions are recorded once in the ledger for the receiver and provider of the transaction. In traditional business systems, the provider keeps their own record in their system of choice. For example, a small retail store might keep its account books using Quicken, while its bank might use an Enterprise Resource Planning (ERP) accounting system to generate monthly statements. The retailer must periodically reconcile its own books to the bank’s statement to ensure everything lines up and is accurate between systems. This reconciliation is avoided with blockchain.

What are the benefits of blockchain?

A number of blockchain technology benefits can be applied in multiple business cases:

- Greater Security — Every block in the chain is encrypted and linked to the blocks before and after it, thereby making it harder to tamper with the information in the chain. This increases the security of the transaction data.

- Increased Trust — Participants (or third-party disrupters) cannot modify or change a transaction once it is recorded because of the decentralization, multiple copies, and multiple stakeholders in the network. This leads to immutable and secure transaction records — and therefore less need of audits.

- Decentralization — Direct interactions between the provider and receiver of the transaction increases trust, eliminates the need for third-party systems and reduces the cost of participation.

- Proof of Ownership — Storage of the asset and transaction on the blockchain serves as an audit log for the asset and its ownership. This allows the provenance or source of assets to be clearly tracked.

Commercial uses of blockchain technology

For the reasons outlined above, blockchain is starting to emerge as an effective technology in many different domains and business applications. We explore a few of the most common and widely accepted cases below.

Currency

Cryptocurrency is the most famous application and the one for which blockchain technology was originally designed. Cryptocurrency (video and explanation available here) is not money as a physical asset but is instead the digital equivalent. Its value only exists in the blockchain network. Cryptocurrencies are examples of public ledgers that anyone can join, contribute to and participate in. They are not regulated by any central bank or agency.

Bitcoin, of course, is the most famous and original cryptocurrency that you can use to buy goods and services. Ethereum, Dogecoin, and Tether are other popular ones. Units of cryptocurrency can be earned through a process called “mining.” Mining involves operating many, many sets of computers together, all running special miner hardware to verify and add transactions (Bitcoin uses the PoW algorithm). Miners are rewarded with cryptocurrency or fees. You can buy, sell and trade your cryptocurrencies in crypto exchanges such as Coinbase or Gemini. Bitcoin even offers a debit card that you can use wherever debit cards are accepted. To preserve their value, cryptocurrencies have an upper bound for the total number of units that can be issued — a cap on value supply. For example, Bitcoin is limited to 21 million units, of over 19.1 million have already been mined.

Food supply chain

Another famous example of blockchain technology being used to solve business problems is in Walmart’s supply chain for a food distribution system based on IBM’s Hyperledger. All kinds of food (fruit, vegetables, grains, protein and dairy) are available from all around the world, but they still need to be sourced from safe, hygienic, and trustworthy producers. Demonstrating the provenance of the food source is a very complex and difficult task. When an illness outbreak occurs due to a food item, it takes a significant amount of time to find the food source and isolate it, time that would be better spent containing the spread of the illness. For example, an FDA investigation of a 2020 E. coli outbreak that affected 40 people across 19 states showed that leafy greens were the most likely source of the infections, but investigators were unable to trace a specific type or brand of leafy greens.

Walmart is a pioneer in experimenting with blockchain to establish a food traceability system to locate the sources of food sold in its stores. Walmart started with mangoes and pork. The baseline for mango sourcing was done by purchasing a packet of sliced mangos at a U.S.-based store and getting the Walmart team to track the farm and producer of that packet. This process, through phone calls and emails, took seven days. Once Walmart created data standards for the barcodes and labels suppliers used and the mango suppliers started using Hyperledger to upload their labels, Walmart was able to trace an individual supplier in just 2.2 seconds by looking into transactions saved in the blockchain for any specific mango using its barcode. Walmart can now trace the origin of over 25 products from five different suppliers.

Copyright protection

With the rapidly expanding use of the internet and, specifically, social media around the world, digital content, such as music, images and videos, can be created and shared very easily. This content can also be replicated or copied very easily to the detriment of the artist or creator. The converse, proving ownership of digital content, also has challenges, especially when attempting to distinguish “inspiration” from “stealing.”

Blockchain can provide an effective mechanism to store the content as an asset, enforce the mechanisms to protect that content and build the trust of ownership of that asset. The blockchain-based copyright management platform Binded provides a simple interface to upload images, register a copyright and monitor image uses on social media sites, such as Instagram and Twitter, to surface instances of infringement. Registering an image on Binder creates a certificate of authenticity, which can be used as a proof of ownership.

Using blockchain to store digital content is the basis of another buzz-creating concept: NFTs. But NFTs will require a separate, dedicated blog to debate their application, investment use case, explosion and crash, all of which occurred in 2022!

Summary

Blockchain technology can be a powerful enabler to increase trust, reduce risk, improve efficiency, reduce reporting burdens and secure both commercial and federal value processing. Its use cases are potentially broad and transformative, particularly as organizations and companies continue to experiment with the technology. While most consumers see blockchain as synonymous with Bitcoin, its potential is far greater.

While business-to-consumer and business-to-business use cases for blockchain are prevalent today, governments are also keen to leverage the distributed ledger to advance agency missions. Our next blog will explore examples of blockchain technology in government applications, both in the U.S. and around the world.

Interested in learning more? Contact us at info@reisystems.com